Chart of the Week – Our National Debt

Thursday, April 20, 2017 | Leave a comment

Source: VisualCapitalist.com

The National Debt Burden

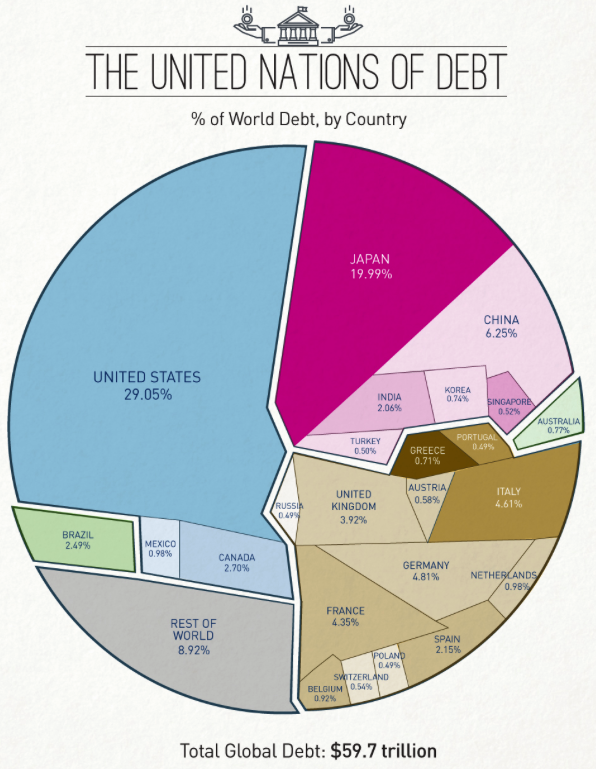

The total U.S. debt has been a delicate topic over the last ten years, as the amount of debt owed by the federal government has ballooned from $5.7 trillion in 2000 to over $19 trillion today. Here is the current U.S. debt down to the penny. This amount of money is difficult to comprehend. (This video does a good job visualizing the debt).

However, it is helpful to view the total public debt relative to the size of our economy. A widely-used measurement of our economy’s size is Gross Domestic Product (GDP). In the year 2000, the U.S. debt was 57.6% of GDP. Today, it has grown to over 104% of GDP—the largest in recent history.

The only other time U.S. debt was greater than this (as a percentage of GDP) was during World War II, when total debt was over 120% of GDP. The subsequent decades of strong U.S. growth after the war relieved our nation from that heavy debt burden. Today’s debt burden has grown to its current level without a major war, but through budget deficits during a relative time of peace.

About two thirds of the total debt is owed to the public through Treasury bills, and bonds. These bonds are owned by individuals, companies, and foreign governments. The other third is called intragovernmental debt. This is money borrowed from federal trust funds to help fund current operations. These trust funds prominently include Social Security and Medicare among others—programs we have all contributed to over our lifetimes and many rely on during retirement.

The rate the United States and many other countries are adding to their public debt is unsustainable. But, in an amusing attempt to lower the U.S. debt, the federal government has given us a way we can help pay it down by directly making “gifts to reduce the public debt”. For those inclined they can do so by going here, although I do not recommend it!

As I help people retire every day, I see some heavily reliant on Social Security for their income, while others have saved and are able to fund much of their income through conservative and safe income strategies using retirement savings. No matter if retirement is 10 year away or just around the corner, any amount of additional savings will greatly help you become more independent from the uncertainty of Social Security and provide more security in retirement.

Thanks for reading,

Nick